- General

- Plugin announcements

-

Pomysły

Pomysły

-1

Post Post Crisis Era to Continue

We’ve talked about the post-post-crisis era as one that is neither risk-off (a period like the financial crisis, when investors shun riskier assets) nor risk-on (a period like the post-crisis period, which we define from March 2009 through November 2014, when investors embrace riskier assets). In a post-post-crisis landscape, markets have a mixed outlook, in which growth is uneven and interest rates remain low.

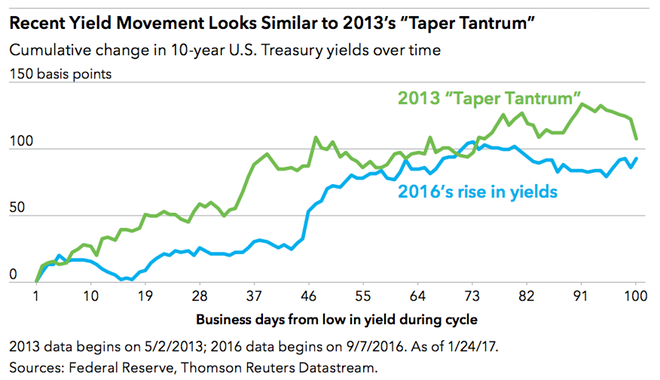

The Taper Tantrum vs. the Recent Rise in Yields

In 2013, the “Taper Tantrum” occurred when the market learned that the US Federal Reserve planned to wind down its quantitative easing program — signaling the end of monetary policy easing and the beginning of a shift toward monetary policy tightening. Consequently, Treasury yields rose 100 basis points over two months. The move higher in yields seemed like a reasonable reaction to such signaling.

The recent move in interest rates also makes sense. The market is taking several things into consideration:

1. Uncertainty about the leadership of the Fed. Janet Yellen’s term as chair is due to end in February 2018. Given the Fed’s dovish policy during her tenure, the market is fearful that Trump will appoint a more hawkish leader who is more eager to raise interest rates and reset the tone.

2. Looser fiscal policy. Trump has championed both lower taxes and higher infrastructure spending. These policies, if implemented, would likely boost gross domestic product and increase the federal budget deficit.

3. Higher inflation prospects. Looser fiscal policy should be a tailwind for inflation. In addition, any protectionist policies, such as amending the North American Free Trade Agreement or implementing tariffs, could cause prices to move higher.

Bond Fundamentals Moving Forward

On one hand, lower taxes, fiscal stimulus and deregulation are all positive factors for riskier assets like stocks (and by extension negative for safer assets like Treasuries). But there are still many uncertainties and other factors that provide reasons to be constructive on fixed income:

1. Uncertain geopolitical backdrop. China is currently growing at a reasonably healthy pace, but that has been aided by a rapid expansion in credit.

2. Uncertain U.S. government policy. To paraphrase Aristotle, the market abhors a vacuum. Following the election, many aspects of government policy are in flux, from spending plans to foreign relations.

3. Risk that fiscal stimulus plans miss their target. The nonpartisan Tax Policy Center’s analysis of Trump’s income tax plan finds that, while high-income taxpayers would enjoy most of his proposed tax savings, middle-income families would receive an average tax cut of $1,000.

4. Risk of a trade war harming growth. If Trump were to follow through on his proposals to increase tariffs on foreign goods, his actions could spiral into a trade war. This would be negative for U.S. GDP growth.

5. Risk of restrictions on immigration hurting economic growth. One little-known fact is that the growth in GDP per capita has trailed total GDP growth by 40% since the financial crisis.

6. Risk of a shock hitting the economy. External shocks are, by nature, difficult to predict but can have wide-ranging effects.

7. Large number of buyers of U.S. government debt. U.S. and foreign pension funds and insurers use Treasuries as an important component of their portfolios, and this shows no sign of changing.

What This Means for Investors

Although it seems very likely to us that the Fed will raise rates gradually in years to come, expected risk-adjusted returns for investing in bonds remain appealing. Recent volatility in the municipal bond market is beginning to present more opportunities for munis*, while healthier realized inflation makes us continue to be supportive of Treasury Inflation-Protected Securities.

Customer support service by UserEcho